When it comes to investing your money, are you confused about how you can get financial advice? What type of financial advisor do you need? What’s the difference between asset management vs wealth management vs financial planning?

Could you take the DIY (Do It Yourself) route instead by improving your financial literacy, with free online investment tips?

In this ultimate guide, we will cover what these different financial advisory services give you. The goal is to help you find the financial professional that suits your needs for your money, whether you want:

- to build a investment portfolio;

- to achieve specific financial goals;

- to plan your long term wealth where your financial resources are put to work for you; or

- to live your dream life and lifestyle, with financial independence.

I’ve been on this Journey

Not so long ago, I was a beginner investor just starting out looking to by my first investment products. More recently, I’ve experienced what it’s like to be a client and recipient of financial advisory services. I’ve also had the fortune to build a successful career working for wealth management firms and in investment banking. So, I can provide multiple perspectives to answer your questions, as I have done in this post.

Context is key. So, we will address the the WHY, WHAT and HOW for hiring a financial advisor by answering the following questions:

Why do you need a financial advisor?

Expert Skills that save you time

Every financial advisor has to be a qualified professional. They are certified and registered to practice and serve you as a client. They have trained for years so they have specialist skills in research and analysis that most of us do not have. This is why it’s worth hiring this professional to look after your affairs and paying for their time.

Regulated to act in your best interest

All financial advisors are also regulated by a government body like the U.S. Securities and Exchange Commission (SEC), the Financial Conduct Authority (FCA) in the UK, the Monetary Authority of Singapore (MAS) or an equivalent financial industry regulatory authority in the client’s country of residence where they are domicile. Financial Regulators set rules to protect investors from losing all their money when taking risks.

Regulations ensure that Financial Advisors are acting in your best interest and there are no conflicts of interest. eg. In some countries like the UK, since 2016, an advisor cannot receive a commission for recommending specific investments to clients.

Regulators mandate a minimum level of due diligence so that your advisor gets to know you. This is the Know Your Customer (KYC) analysis process. To make investment recommendations, your advisor has to validate your suitability for their services and their advice. They must conduct a risk assessment to understand your risk tolerance, to find products and services with the best fit.

What do financial advisors charge? Are there different costs for Financial Advice?

The first question to ask before hiring a financial advisor is whether you can you afford one. Just because you think you need an advisor, doesn’t mean that they can serve you. Advice from a skilled expert can be expensive.

There are minimum fees for most financial advisory services. So, let’s look at the costs for Financial Planning vs Asset Management vs Wealth Management services:

*Costs listed are based on public information available as at January 2023. Updates will be logged here. Fees are mostly listed in USD or GBP for the US and UK market and may vary for other countries.

Financial Planning Costs*

In the US, you need a minimum of $50,000 (USD) in investable cash to access a Financial Planner for investing advice. This is about £30,000 (GPB) in the UK.

The is also a minimum flat fee of $1000 or about £800 to create a Financial Plan for you. This includes a meeting over several hours to review your financial situation, and set your financial goals. After this, a financial plan or report is generated with some advice or recommendations for next steps.

Some financial planners may recommend their own affiliated mutual funds for you to invest in. These mutual funds charge a 1% fee per annum of your total investment in the fund. Your investment is known as your ‘Assets Under Management’ (AUM).

Other Financial Planners may charge retainer fees which range from $2000-5000 per year. When a retainer is charged, then they may not be any AUM fees.

Is Financial Planning Worth It?

Can both the client and the advisor get a return on investment (ROI) from working together?

ROI is the main reason why there are minimum thresholds for investing.

Is there ROI for the client?

If a client only had $10,000 to invest, it is difficult to justify a $1000 at 10%. It is difficult to grow your investments by 10% given that average yearly returns for most investments is just 7-8%.

While it’s not impossible to achieve a 10% gain in 1 year timeframe, there is no guarantee of any growth. Gains of this size and greater require strong market conditions.

Timing the market is obviously difficult and not recommended practice. You risk loosing all your money as a beginner investor if you go all in.

Taking such a huge risk with a beginner investor, is not acting in the client’s best interest and violates regulation.

Is there ROI for the Financial Planner?

Unfortunately, it is also difficult to justify an ROI for the advisor’s time for relatively small fees. Eg. $100 in AUM fees from a $10,000 investment plus an initial $1000 plan.

A small fee of just $1,100 doesn’t give the advisor an incentive to spend hours on a comprehensive plan.

Most financial planners seek clients who wish to engage their services over a longer term on a retainer basis. There is an ongoing relationship and higher regular fees to provide a regular income for the advisor. This beats doing a lot of work on one-off services, for a mere $1000.

Asset Management Costs

Asset Management covers an array of investment services including:

- ROBO-Advisors that are available directly to ordinary investors with a $1 investment

- Mutual funds charging fees from 0.2% to 2%

- Bespoke Portfolio Management services from portfolio managers who charge from 1-2%

Fees may be higher for access to more complex products or investment vehicles across the primary or secondary markets. eg. Hedge funds.

Usually, Asset Management charges are also on-top of existing Wealth Management service charges.

Wealth Management Costs

Serving the Mass Affluent vs the Super Rich

In some rare cases, you can access a wealth manager with a minimum investment of $500,000 in liquid cash only. Wealth Management firms classify their clients with less than $1million of liquid cash to invest as the “Mass Affluent”.

Wealth Management firms specialize in helping the rich only and tend to only serve people with in excess of $1million in liquid assets or cash to invest. The industry classifies those with $1-5million as HNW individuals. Eg. You need $1 million in investible cash to open an account Coutts, a Private Bank that manages the money for the Royal Family of England.

Some Wealth Managers only work with the super rich known as the Very High Network (VHNW) who have between $5-30million or the Ultra High-Net-Worth (UHNW) with at least 30 million to invest. UHNW clients may be the head of a family office or trust, with many millions if not billions. Eg. The Wealth Management division of Goldman Sachs has a minimum threshold of 20million in AUM for its new clients.

Wealth Management firms typically charge between 1% to 1.5% in annual fees of total assets under management (AUM).

1% of 30million is $300,000 in fees per year. With such high earning potential, nothing is too much trouble when it comes too serving UHNW clients 😃.

Wealth Managers with Services for the Mass Affluent

Of course, there are smaller or boutique wealth management firms that may offer better minimum investments to work with their advisors. These tend to be Investment Management firms or Asset Management firms that offer Financial Planning add-ons to their ‘Mass Affluent’ clients.

Anyone with $100,000 to $1million to invest is classified as a ‘Mass Affluent’ client across the Financial Services Industry. Obviously, amongst this very big pool of clients is your next millionaire HNW individual, whom different Wealth Managers compete for. This is why Advisors both big and small, may begin to compete for these clients. They compete through a different price structure and smaller investments thresholds, as well as other fees for on-off projects.

Some Wealth Management services designed for the Mass Affluent include:

- Managed Portfolio Services starting from about $50,000 AUM

- Discretionary Portfolio Management services starting from $250,000 AUM

- One-off fees of $1000-3000 for a financial plan

- Hourly rates or project rates similar to lawyer or attorney fees and CFAs fees

- Flat fee retainers between $2000-8000 per year instead of AUM fees

Many Wealth Management firms are also building their own ROBO-Advisor apps to serve Mass Affluent clients. After all, it’s smart to monitor the size of a digital investment account for an opportunity to upgrade the client to full Wealth Management services.

What Is the Best Path for beginner investors?

What are your options… if you can’t afford a financial advisor because you’re just getting started?

For those at the beginning of their investment journey who are taking that first step into investing, you should focus on just 3 Steps:

🎁 BONUS TIPS: Avoid get rich quick schemes like a random stock selection or a recommendation from a YouTuber to buy specific CRYPTOs. Just let the power of the COMPOUND EFFECT do its magic naturally and organically so you are making money in your sleep over 10, 20 or 30 years.

Mastering these three steps alone will make you a fairly component DIY investor capable of becoming a millionaire. There are also other beginner friendly DIY investing routes such as investing directly in stocks, buying real estate or even purchasing precious metals like Gold.

Check out our “Investing for beginners” post series and video playlist to help you build your Financial Literacy.

What is Financial Planning? What services do Financial Planners provide?

Financial Planning is the process to create a plan for your money, and how it will support your life and your happiness.

The truth is… anyone can create a financial plan, but not everyone knows how to create a good one.

A good Financial Plan will have strategies and actionable steps that will deliver the outcomes to meet your financial goals.

When it comes to defining strategies for specific financial goals, you may need the help of a qualified Financial Planner. Especially if you aren’t educated in these specialist skills that can take many years of training and experience to acquire.

A Financial Planner can help you to create a comprehensive plan for managing your money, your life and our happiness. More importantly they can also reset this plan with you when things go wrong or change – that’s life. C’est la vie!

Financial Planning Services

The types of Financial Planning services included in different Financial Plans, and provided by a Financial Planner include:

Budgeting

Budgeting is how you manage your cashflow in order to have a surplus in funds for saving and investing. You get a surplus by subtracting your income coming in, minus your outgoings or expenses. It involves specific steps to monitor your expenses, so you are spending it wisely, to give that surplus. You may need to develop a budgeting strategy to manage your personal financial needs or your family’s overall financial situation. Your needs and wants are what you turn into your financial goals.

Debt management

Debt management involves specific strategies and implementable steps to help you pay off your bad debts faster. The goal is to give you surplus funds by reducing your expenses from interest payments on the debt you owe. It may also involve improving your credit score so you can get a loan. There many forms of loans like your credit card debt, your mortgage, student loans, car loans and business loans. You can even borrow money to fund your investments, such as to buy stocks and to buy and rental property. Debt that supports your investments is known as good debt, because it gives you “Leverage” – an advance financial strategy.

Saving and/or Insurance for life events

Major life events can require huge sums of money, so you need to plan for them in advance. Examples of big life events that can cost 10s, 1000s and 100s of thousands, include:

- a wedding;

- going to college and university;

- medical treatments for health problems;

- fertility treatments and family planning;

- medical care in your old age; and

- funerals;

Saving for these big life events over a period of time, may not be enough to protect losses from the effects of inflation. There are specialist insurance plans to protect your savings with fixed payouts for specific life events. Some of these specialist insurance products may only be available via financial planners.

Investment Advice & Investment Management

Investing is how you grow your overall net worth by putting your money to work for you. This involves buying, selling and holding your money in financial assets to generate an income as well as appreciating in value. When an asset increases in value, you net a capital gain over the initial cost of the asset.

Investing is how you become wealthier and even rich but it is highly volatile. Capital gains and income are not guaranteed. You risk losing your money if your held financial asset decreases in value and you are forced to sell. Some asset classes may yield no income at all or so little income that all profits are eaten away by inflation.

As the past performance of any asset never indicates future performance, investing without the skills and time to study market conditions in different economies introduces risk. So, how do you mitigate the financial risks in a portfolio?

This is why hiring a Financial Planner can help, because they can measure your risk tolerance properly. They will do this prior to setting up an investment plan that is aligned to your financial goals. They may also assist with tax planning to maximise your use of retirement accounts. This is useful because your tax savings from your investments, is more money to reinvest and grow your portfolio. Investment advice should also include strategies to diversify your portfolio as this will mitigate risks for you as your investment portfolio grows. So, your Investment Manager may induce you to other asset classes like beyond stocks and into bonds, commodities, etc…

Retirement planning

Retirement planning involves managing your cashflow, savings and investments to generate a passive income for your desired lifestyle in retirement.

So, how much money do you need to retire? When do you want to retire? What kind of lifestyle do you want, when you retire? These are all financial goals that you need to set, as part of retirement planning.

Society including the laws in many countries dictate that we all work until a certain age, before retirement. In most countries, this is usually from your mid-50 to late 60s.

Of course you may want to or need to retire earlier in your 30s and 40s. This is what the FIRE Movement promotes. FIRE stands for Financial Independence Retire Early.

Whatever your age, to stop working, you must replace your regular income from your day job, with other income. So, you have to find ways to generate passive income. A financial planner can help you to maximize your passive income from your retirement accounts.

Regular savings into specific tax-efficient retirement accounts is supported and/or mandated in many countries. eg. 401k and ROTH IRA in the US, ISA and SIPP in the UK, RRSP in Canada, Superannuation in Australia and CPF in Singapore. These retirement accounts are tax -efficient because you pay less or no tax on any income and capital gains. So, you can use the funds in these accounts to invest in stocks and bonds. In Singapore, you can even buy real estate with your CPF.

Estate planning

Estate planning is how you can pass your assets and legacy to family, friends or organizations upon your death. So, who gets all your money including any insurance payouts.

Some wealthy people actually plan how they want to distribute their assets before their death and as soon they have children.

A financial planner can help you to develop a plan for this, including drawing a will with a solicitor. They can recommend an executor to manage your affaires when you are dead. They can also help to set up a trust to help you reduce inheritance tax.

Tax planning

Should you be seeking tax advice from a Financial Planner or an Accountant or a Chartered Financial Analyst (CFA)? That depends on your different income sources and investments and when you wish to retire. Do you have assets across multiple countries with different laws?

Tax planning is not just hiring someone to complete a simple tax return annually.

The more complicated your financial situation, and the more investments you have, where you want to maximize your tax savings to give you more income… then the more likely it is that you will require a specialist to manage this minefield of changing rules or laws, while protecting and growing your investments and your wealth.

An integrated financial plan vs independent financial strategies

With so many financial advisory services involved in Financial Planning, could this all really be handled by one individual? There are so many specialisms to train for.

This is why most Financial Planners work in a practice where they may involve other colleagues with different specializations to work on the different aspects of a client’s bespoke Financial Plan.

Of course, you can also access many of these financial advisory services independently and directly on a one-off basis, but then you will lose the benefit of having a comprehensive approach with an integrated set of strategies that are setup to maximize your long term wealth as well as supporting your overall Financial Wellbeing.

The question is whether your current financial situation requires the integrated plan, just yet. A professional financial planner will use the appropriate qualification criteria to help you determine your fit for their services. Most offer an introductory 30 minutes chat, which is usually complimentary to determine this fit.

What is Asset Management? What services do Asset Managers provide?

In the Financial World:

Asset Management is a specialist financial service offered primarily via Investment Banks and Wealth Management firms to corporations, institutions and wealthy individuals to help them manage their investments in order to grow its total value.

Asset Managers are investment advisers who produce an investment strategy to help their clients buy, sell, and hold a portfolio of assets according to a specific asset allocation. They conduct ongoing risk-return analysis to set up an investment strategy that matches the risk profile versus specific financial growth targets for their client, and incorporating different market conditions.

In reality, Asset Management is more than a financial advisory service as it involves order management and execution of trades on behalf of the client. The Asset Manager is trading at their own discretion to continuously rebalance a client’s portfolio to give it the most optimal asset allocation. When they do this, Asset managers are fiduciary advisors with fiduciary responsibilities that are heavily regulated by many government bodies. So, they have to be a registered investment advisor.

An Asset Manager will consider their client’s risk profile or tolerance and trade different asset classes, including stocks, bonds, as well as other assets like REITs or Commercial Real Estate and Commodities, in an investment portfolio. They may also provide more complex products including derivatives, currency hedging, private equity and as Options and Futures.

Many asset managers are beginning to introduce Cryptocurrencies and NFTs into their clients’ portfolios where allowed by regulation.

Types of Asset Managers

Portfolio Managers

A Portfolio Manager is a top asset manager with many years of experience managing bespoke investment portfolios for clients.

In Wealth Management firms and Corporate & Investment Banks, Portfolio Managers are drawn in to manage a rich or large client’s investments via a Relationship Manager.

As the goal of a portfolio manager is to maximize investment growth, so more risk is taken. This involves the introduction of more complex investment products, as well as more complex trading in the primary and secondary market across different asset classes.

Amongst the asset management profession, Portfolio Managers are typically paid the most because they produce the highest ROI for their clients as well as their employers… the banks and financial firms that hire them. Salaries start in the 100,000s and can go up to many millions, where the Portfolio Manager is themselves getting a commission from the 1% of AUM and in many cases up to 2% of AUM in fees taken from the clients portfolio yearly.

Many Portfolio Managers also work with Financial Planners and Brokers or Brokerage Platforms, specially when it comes to offering ROBO-Advisor services or getting involved in the management of Mutual Funds.

Personal Experience

I tend to do my own Portfolio Management as a DIY investor because I have strong Financial Literacy. In the UK, I use online brokers like Hargreaves Lansdown and Trading 212 to management my investment portfolio where I have a mix of funds and direct trades or stock purchases.

I use Trading 212 for direct trades along with other StockScanner apps to help me learn about specific stocks and their underlying financials or company performance metrics.

I like to use Hargreaves Lansdown for regular saving and investments to maximise dollar cost averaging, because it also offers a marketplace of banks and with high interest yielding cash management accounts as well as access to EFTs, Index Fund and Mutual in many international markets like the US, Japan or Emerging Markets. So, it is a good place for parking your money while you’re looking for the best time to buy and sell or to diversify globally into other markets or economies.

I also have brokerage accounts like ETrade in Australia and in Singapore too, because I use live in these countries.

ROBO Advisors

The more recent growth of ROBO-Advisors which are online platforms supported by asset managers or an AI algorithm that has been coded and trained to act as an asset manager, has made Asset Management services more accessible to regular investors, and especially the MASS Affluent.

In fact, it is now possible to invest via a ROBO Advisor platform for as little as $1, or in most cases a minimum investment of $100. Typical asset management fees taken are on the lower end of the scale at 0.2%. So, ROBO-Advisors are similar from this perspective to passively managed mutual funds.

In the US, Robo Advisors include independent apps such as SOfi and Betterman as well as those offered via traditional brokerage houses like Vanguard, Fidelity or Banks like Morgan Stanley who own Etrade.

With the strength of London as a Global Financial Services hub and a leader in Fintech, the UK has many Brokerage apps, such as Moneyfarm, Nutmeg, InvestEngine, Wealthify, etc… with their own ROBO Advisor services.

Personal Experience

I personally invest with InvestEngine where I have a mix of ETFs, Index Funds, and ROBO-Advisor led Mutual Funds. I was attracted to InvestEngine because of the BONUS offer of free money (£100) to open a new account with them provided I invested a minimum of $1000. So, it’s a good idea to keep looking out for these sorts of deal and offers – who doesn’t want free money.

What is Wealth Management? What are private wealth management services?

Wealth describes the Net Worth of affluent people comprising the total value of their assets minus their liabilities, and the continuous growth potential of their portfolio of assets.

As implied by the title…

Wealth Management is a set of investment management services for managing people’s wealth over the long term including money that can be passed to future generations.

Private wealth management services are typically exclusively available to the rich only, because only the rich can afford the higher fees for a more holistic set of financial planning services along with an asset management service.

So, one way to view Wealth Management is via this formula:

Wealth Management = Asset Management + Financial Planning

In Wealth Management firms, affluent clients are served by a high touch Relationship Manager who acts as their wealth advisor, and is thus responsible for every aspect of wealth management including advice for managing an affluent lifestyle. So, the Relationship Manager’s job is to gather all relevance of any information while connecting the right specialists, including Financial Planners and an Asset Manager to support their client’s maintenance of their overall wealth in the long term.

How does a financial advisor work with me? What is the process?

As financial advisors need information about you and what kind of lifestyle you want to lead, the process of working with you as a client should always start with the basics of the Financial Planning process. So think of your Financial Plan as containing the inputs for your Investment Management and Wealth Management strategies, where the outputs are produced.

Financial Planning Process → Financial Advisory Process

The Financial Planning process steps to support further financial advisory involve:

To sum up, there are 5 steps in the financial advisory process that need to work together to give you a transformation with your money, life and your happiness. More importantly, I hope you can see that these 5 steps are more effective because they involve defining S.M.A.R.T. Financial Goals that you can implement.

If you want to learn how to set S.M.A.R.T. Financial Goal for yourself (DIY), check out my youtube video where I walk through a personal example – “To be Mortgage Free” 👇

Financial Plan vs Financial Game Plan

Every Financial Plan should have short-term, medium-term and long-term Financial Goals. More importantly, these goals need to be S.M.A.R.T. because that is how you can break down your goals into projects and actionable activities. In addition, you should include your risk profile and tolerance to help inform the strategies and actions that will get defined through this Financial Plan.

This is why when you choose to work with an independent financial advisor on a one-of basis, you need to pay a fee upfront for this work, which is to create your first Financial Plan. When working with a Wealth Management firm, this plan is also developed by your Relationship Manager up front in order to direct the other wealth management services to work for you.

Only once you have this starter Financial Plan, can your financial advisor proceed to offer you advice that incorporates specific investment strategies.

To clarify, it is the inclusion of these strategies and the implementation activities that will deliver the transformations for you as the client when this Financial Plan turns into a more fully fledged Financial Game Plan.

So, the formula is:

Financial Plan + strategies + implementation steps = Financial Game Plan

If you’re looking for an initial Financial Plan and Financial Game Plan template or cheat sheet that you can use for yourself (DIY), check out my YouTube video on How to achieve Financial Independence in 12 months.

Managing Relationships and Investments Ongoing

The process for New Financial Plans

When you engage a Financial Planner, or Wealth Management Relationship Manager for the first time, there are 3 stages to expect before they can commence taking care of your investments…

Firstly, they will create your initial Financial Plan comprised of your Financial Goals. Secondly, they will bring in the relevant experts to help you extend your Financial Plan into a Financial Game Plan. Subsequently or thirdly, they will set up your investment accounts ready for trading.

Meanwhile, your designated Asset Manager begins to assess your suitability to specific financial strategies. In addition, they will consider the right asset allocation across your investment portfolis. Subsequently, when your investment accounts are open and ready, then they can commence transacting and/or trading on your behalf.

Adjusting Financial Plans Annually

After your initial set-up is complete, your Financial Advisor will serve you on a ongoing basis, by reviewing your Financial plan and Game plan with you at least yearly, in a pre-arrange annual review.

Following each annual review, the full financial advisory process repeats itself, as the other experts are brought in to act or implement for you, as your wealth continues to grow.

More importantly, your Financial Advisor and the relevant experts in your Financial Advisory or Wealth Management team will adjust things based on any new financial goals or life events that you have.

At this point, you should be able to lead the lifestyle as described in your Financial Plan, be that a luxury lifestyle as you have Financial Independence or Freedom, or you may have other business and entrepreneurial pursuits.

How can financial advisors support business owners and entrepreneurs?

Business owners and entrepreneurs will have business goals that can be incorporated into their financial plan as their own financial goals by their financial advisor.

This is usually simply another add-on service for those who don’t yet have the funds to utilize a Wealth Management firm to help them manage their financial affairs more holistically.

Businesses privately owned that are not listed on the stock market are considered as assets too inside of a holistic Wealth Management Financial Plan and where relevant, and a relationship manager may choose to bring in additional expertise such as a Private Equity manager or M&A investment bankers to help the business owner grow their business through buying other businesses or to sell these businesses.

These sorts of services are at the very high end of the Wealth Management service for their most valuable clients. A.k.a. big business clients who cross over through their businesses into engaging Corporate and Investment Banking services.

What value or ROI does using a Financial Advisor really return Vs the DIY route?

When choosing between Asset Management vs Wealth Management vs Financial Planning services, it is difficult to use ROI with exact numerical values as returns vary year-on-year based on varying market conditions. In addition all investors will have their own individual financial goals and different levels of investment.

Financial Advisor Measures of Value

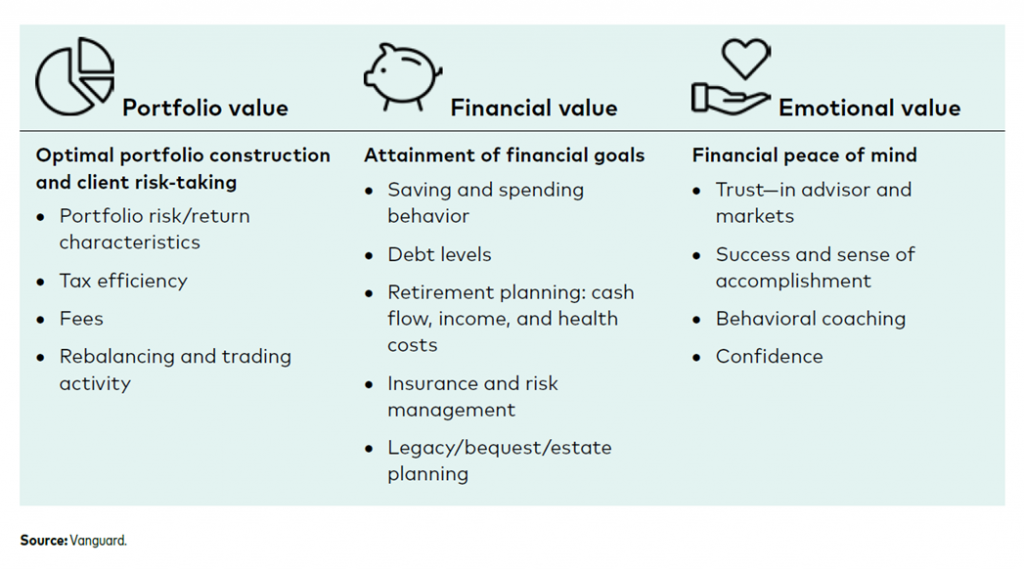

A 2021 study from Vanguard has shown how Portfolio Value, Financial value and Emotional Value have all increased or are higher from having financial advisor involvement, compared to investors who took the DIY route.

Portfolio value measures the financial advisor’s role in constructing an optimal asset allocation according to risk in the client’s portfolio.

The results of these studies have indicated a higher perceived value in returns from human advisor involvement at up to 5% in portfolio value for investors with a medium size of $1million in their portfolios.

Financial value measures the financial advisor’s role in the client attaining their financial goals.

In the same report, it was perceived that financial advisor involvement versus having no advisor resulting in an extra $160,000 or 16% extra in value where the financial goal was to have investment accounts of $1million in value.

Finally, there was little doubt that the use of financial advisors and especially human advisors provided sustainable peace of mind for investors with this measure increasing by 56% to 80% compared to the 24% as experienced by investors who did not use financial human advisors. Interestingly, there was only a 12% increase in peace of mind or investor confidence from using digital advice.

The report also indicated an overall 55:45 ratio in the functional value vs emotion value of advice, with participants associating 45% of the value of advice with the emotional aspect of the relationship.

Financial Advisor Benefits

Another study also by Vanguard found that advisers added ‘alpha’ to investor’s portfolios in the following ways:

- Improve risk levels in portfolios to appropriate values

- Elimination of large cash holdings in portfolios

- Increase diversification into foreign or other markets thus eliminating a home bias

- Reduced individual stock risk

- Avoidance of market timing errors from improved behavioral coaching

- Improved Tax management

- Optimisation of income drawdowns from older investors

- Getting new clients to start investing

Does DIY Investing Work?

This study also showed that DIY investors who have the time, willingness and ability to learn about investing and managing their own portfolios using digital tools, were less likely to benefit from employing a human financial adviser, which just goes to show that the DIY route can work as long as you have the time, willingness and the ability to learn.

Time Is Money. Don’t waste time getting started

So, do you have the time, willingness and ability to learn financial literacy so you can grown your own wealth, or should you consider a financial advisor since is time is money and you’d rather be spending your time on other things that bring you joy in your life? If you prefer to pay for help, then the question is what kind of financial services can you access now, and what are your needs and wants. This will determine if you need Asset Management vs Wealth Management vs Financial Planning, at the current time. Whatever your decision, the key is to start investing as soon as you can and start young, and go DIY if you have to, as again, TIME IS MONEY.

To explore the DIY path, you can certainly get started by building your Financial Life Plan for the next year, starting with conducting a Money, Life and Happiness Audit👇

Financial Life Planning Workbook

+ Money-Life-Happiness Audit

Grab the free advanced MoneyBrain action plan worksheets to help you start living with Financial Independence in the next 12 months.

You’ll also receive monthly MoneyBrain emails with PRO tips + other exclusive offers to help you make your time and money work for you.

Your information is 100% secure and will never be shared with anyone.

You can unsubscribe (opt out) at any time.